Articles

Mathematics Behind Automated Market Makers

Mathematical foundation for more efficient DEX markets: liquid, fast & profitable

Automated Market Makers (AMMs) represent a foundational technology in decentralized finance (DeFi), allowing for asset trading without traditional market makers. Instead of using an order book, AMMs utilize mathematical formulas to determine the price of assets based on the supply and demand within a given liquidity pool.

AMMs transform DeFi trading by providing liquidity algorithmically. While they enhance accessibility and inclusivity, they also introduce challenges such as impermanent loss and arbitrage vulnerabilities. Despite these issues, the robust fundamentals of AMM offer possibilities to address these gaps. 😇

🏦 Terminology

Automated Market Making AMM

New alternative structure for electronic trading; they are blockchain wallets which can hold crypto assets, but whose behavior is determined fully by blockchain code

Limit Order Book LOB

Traditional structure in electronic trading based on trade orders

Centralized Exchange CEX

Supervised entity for placing market orders

Decentralized Exchange DEX

Trust-less exchange on smart contracts on blockchain

Liquidity Provider LP

Animator of the market reducing slippage cost

Loss-Versus-Rebalancing LVR

Costs incurred by AMM LPs due to triggered prices by informed arbitrageurs

Miner Extractable Value MEV

Arbitrage profits for AMM

Uniswap UNI

DEX operating on the Ethereum blockchain

Sushiswap SUSHI

Uniswap with SUSHI token

Arbitrageur

Market participant profiting on price discrepancies in markets without market risk

Market Risk

Losses in positions from market price movements

Liquidity

Price availability for transactions without significant price changes

Marginal Liquidity

Liquidity levels corresponding to AMM's demand curve

🍹 Strategy types

Rebalancing Strategy

Strategy trading at CEX prices and holds the same quantity as in AMM

Rebalancing Arbitrage

Strategy that profits from price adjustments in CEX and CFMM

Delta-Hedging

Strategy that offsets the market risk by shorting the rebalancing strategy

Sandwich Attack

Strategy that manipulates prices by placing Bids & Asks on both sides

Sniping

Strategy of exploiting momentarily favorable conditions in trading

😫 Cost types

Price Slippage

Cost between spot and strike prices (contributing to LVR)

Impermanent Loss

Cost of divergence between the AMM's price and the market price (similar to LVR)

Convexity Cost

Cost of predefined loss in trading function (due to curvature)

Predictable Loss

Cost of expected loss from trading, including convexity cost

Fees

Costs of transactions, including gas fees

Gas Fees

Costs of computing energy for transactions

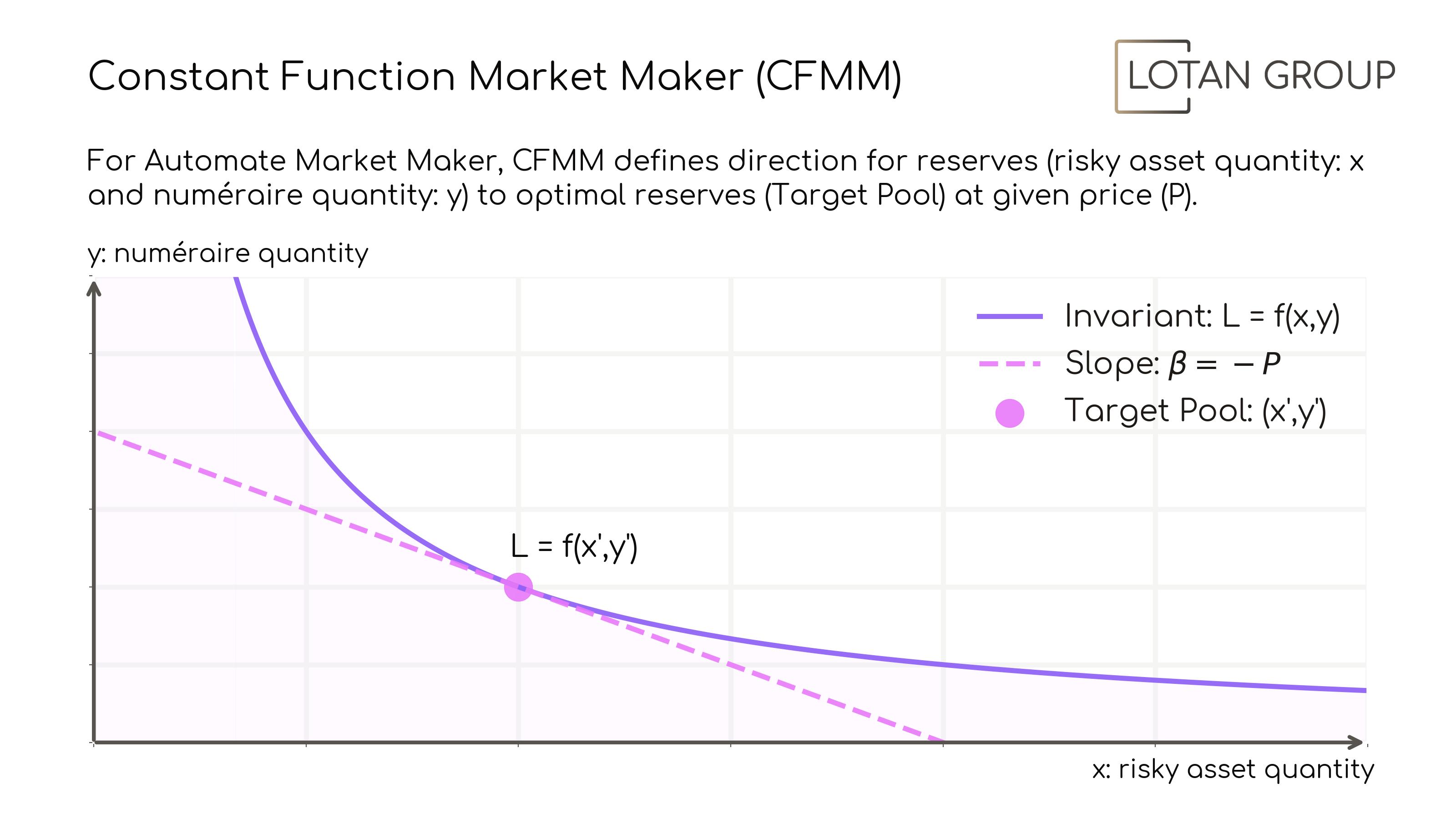

📏 Equations and further definitions

🦚 Examples of CFMM

Company Number: 8992639286 |

VAT-5UE: PL8992639286 |

Registered: Poland, Wrocław 53-129 Sudecka Str. 114

© 2024 Lotan Group. By using our service, you accept our terms and conditions.